my cash now payday loans

The latest AI Apps Seek to Open Equity to split A home Gridlock

The result is new cycle already determining the present landscape, where residents end up being secured in, unwilling to sell and provide right up the advantageous mortgage costs, if you’re consumers try deterred from the high will cost you.

HomeLight maker and you will Chief executive officer Drew Uher told PYMNTS’ Karen Webster you to definitely fake cleverness could help discover collateral and you can put movement in order to a beneficial static industry.

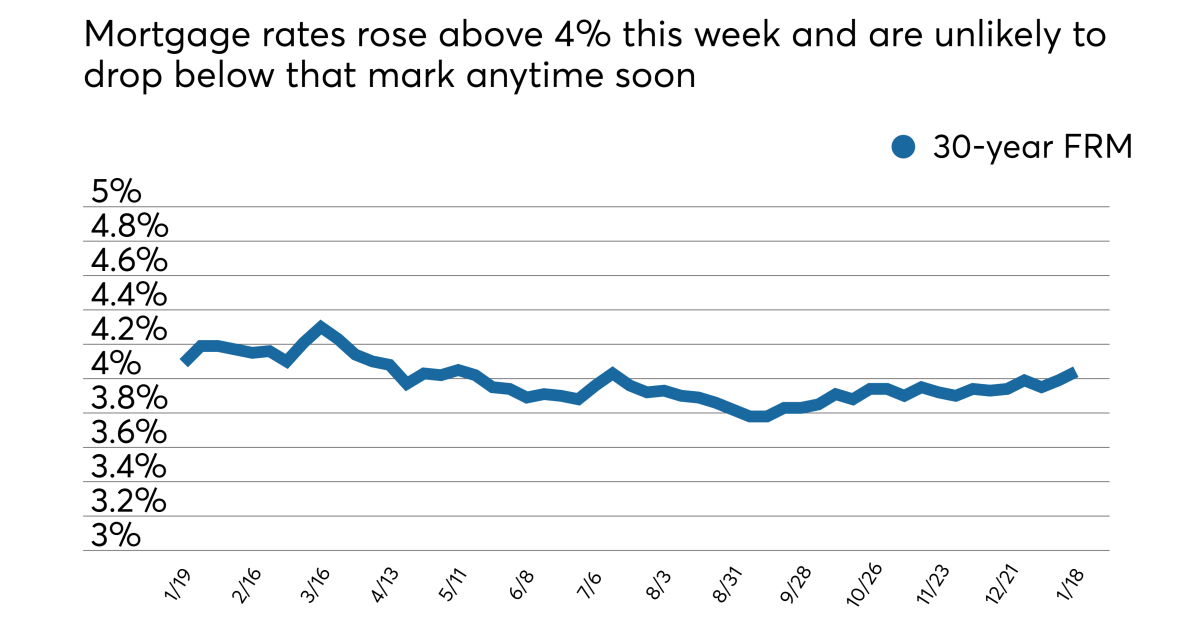

Of numerous home owners try trapped inside their land because of lowest-interest rate mortgages, incapable of sell even if lives factors might strongly recommend they want to. Alternatively, potential buyers are being listed out-by large mortgage pricing and stagnant houses costs. It consolidation provides led to a slowdown in the industry, having deal amounts during the its lowest once the middle-90s, exceeding probably the downturn viewed in 2008 overall economy, Uher told you.

It’s chaos available, the guy informed me. You’ll find an incredible number of property owners just who very own a house and have this amazing low interest to their mortgage. This means that, they think like they can’t promote.

Towards the visitors front side, cost stays a major procedure. Home prices features stayed highest, additionally the diving during the financial prices makes investment a house pick costly than ever before. People has actually less options, and manufacturers was hesitant to number their homes in an industry in which they understand the fresh to shop for pool is constrained. It offers led to what Uher known as a whole bloodbath within the last couple of years for those on the real estate industry.

Transaction volumes provides plummeted, undertaking a difficult ecosystem the real deal estate professionals off agents so you can mortgage companies that rely on hobby in the business to thrive. Home prices on their own, simultaneously, remain at a more impressive range, meaning domestic a home stays a valuable asset, at the least of these lucky enough to have their residence.

Having home owners stuck in cases like this, who want to sell its most recent household and buy an alternative domestic, regardless of the industry, he is commonly littered with the trouble which they normally you need to sell its newest household first in acquisition to afford the fresh new brand new home, informed me Uher.

The fresh new AI Software Aim to Open Equity to split Home Gridlock

But in the payday loan Del Norte current markets, making a deal toward a different household contingent toward selling a keen present home is commonly a non-starter, the guy extra. Additional options, like promoting and you may local rental straight back the house or property to possess a time, otherwise moving into a rental briefly, cost a lot and you may disruptive.

As the residents get a hold of a method to beat the difficulties off rising home loan prices and you can stagnant home values, the newest digital situations can take advantage of a task in aiding all of them reach the a home goals.

Of many property owners must unlock the new security using their current domestic to place to your the latest deposit, said Uher, detailing that HomeLight’s own Buy Before you could Sell solution was created and make investing home a whole lot more accessible by the streamlining usually complex and you can go out-sipping process and you may giving even more flexibility and you can openness.

The new Buy Before you Promote program simplifies the conventional a house buy techniques by allowing property owners purchasing their new domestic before selling their newest one. This decreases the big date, costs and fret employed in dealing with each other transactions immediately.

Controlling Field Threats That have AI-Motivated Abilities

A button invention for the HomeLight’s Purchase Before you Offer product is their accessibility AI. The applying is an AI-first unit, having fun with AI regarding entire process, from home valuation to customer qualification. Predicated on Uher, AI can be used to add instant decisioning about how precisely far collateral a resident can be discover off their latest possessions, considering real-date business study.

We have been available today within the 47 claims, therefore, the bulk of this new U.S., the guy said. Among the many things we’ve read is the fact this will be, in one single means, a lender-centered device.

For mortgage brokers and you will financing officials, this technology was integrated in to their present equipment, such as for instance financing origination options and you can section-of-deals assistance. So it consolidation allows mortgage officers to provide instantaneous, data-supported knowledge so you can readers how much equity they could access because of their brand new home get.

Uher highlighted the necessity of AI into the streamlining this action, reducing the need for lengthy valuations and you will underwriting techniques, and making certain that deals disperse efficiently and quickly.

Looking ahead, the guy said he notices AI-inspired development since the an essential unit in assisting property owners browse the latest demands of shopping for yet another family during the a leading-rate, high-rates ecosystem.

The brand new pleased road try everything is treated by the technical alone, and also the human beings is introduced to cope with very unconventional otherwise unusual times, he told you.