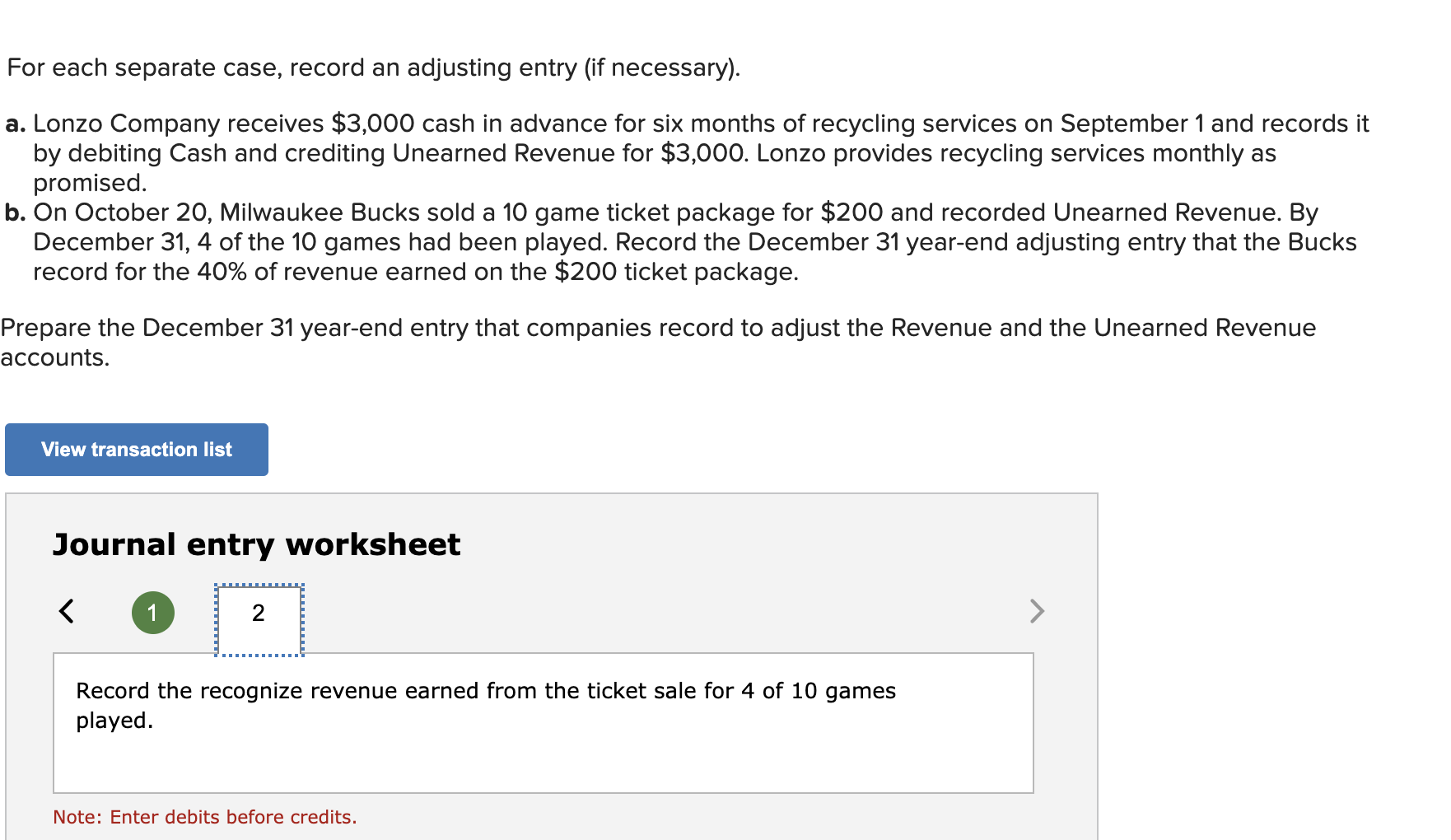

paydayloanalabama.com+belgreen payday loan instant funding no credit check

Are a property Security Financing wise?

Skylar Clarine try a fact-checker and specialist during the personal money which have various experience in addition to veterinary technology and flick degree.

Household guarantee hit a record a lot of $9.9 trillion at the end of 2021. When you are one of the main People in the us that happen to be currently sitting to your an ocean away from unexploited home security, you’re likely bringing adverts promising one to sign up for a property guarantee loan check loans Belgreen AL. Is just one a good idea for you?

Secret Takeaways

- A home guarantee mortgage allows you to borrow a lump sum of money up against their residence’s guarantee and you may pay it back more than time having repaired monthly installments.

- A home security mortgage are a good idea whenever regularly raise your house’s worthy of.

- A property security financing is actually a bad idea when accustomed spend frivolously.

Just how House Security Fund Performs

A property security financing is actually a loan enabling one take out a-one-time lump sum and pay it back on a fixed attention price with equivalent monthly obligations over a decided-upon time period. Home security fund offer all the way down interest rates than other different personal debt, for example credit cards and personal finance, because they make use of the collateral you really have in your home just like the guarantee toward mortgage.

Home security financing, home collateral lines of credit (HELOCs), reverse mortgage loans, and cash-away refinances are typical getting cash by the credit up against your home. By using the home’s security similar to this, you take toward a couple fundamental threats:

- If you fail to manage to pay your loan(s) straight back, you can clean out your property in the a foreclosure.

- When your home’s worth decreases, you could potentially getting under water on your own mortgage(s). Therefore, you simply will not manage to offer your property rather than bringing good financial losses.

When a property Security Loan Are a good idea

Property guarantee mortgage should be smart when used to pay for a task that can physically improve house’s guarantee. Making use of their home’s collateral using a loan decreases the equity you may have of your property through to the loan are reduced. Utilizing the financing to find a job that boost the home’s value might help mitigate the risk of the borrowed funds.

A home guarantee mortgage was a comparatively good notion about a face-to-face mortgage while they have dramatically reduced charges, nevertheless they nevertheless should be put as long as funding a venture that may improve house’s well worth.

Using a property security loan to help you combine large-notice financial obligation are sensible if you have the discipline and altered circumstances to pay off the home equity financing on time. Ensure that you are handling one fundamental patterns that may enjoys was the cause of higher balance regarding debt, instance overspending as well, and that means you don’t find yourself caught for the a personal debt spiral.

When property Guarantee Loan Is an awful idea

Generally speaking, a property collateral loan was an awful idea when it is useful for one thing besides something which often actually raise your home’s value. Property security loan are an especially crappy tip whenever put frivolously. Don’t use a house equity loan to fund a life you to your income cannot sustain. If you’re unable to afford luxury food, trucks, and you will vacations on the earnings, cannot erode their house’s security in order to temporarily live that lifetime.

Try a house guarantee loan or a property guarantee distinctive line of borrowing (HELOC) a better tip?

Each other property collateral mortgage and you can a home guarantee distinct borrowing (HELOC) borrow on your house’s security and you can hold the same dangers. Good HELOC enjoys a varying interest, whereas property equity loan almost always provides a fixed focus rates. Whenever rates was ascending, it’s a good idea to get a property security loan rather than hold a premier balance to the an excellent HELOC. An effective HELOC will likely be a much better idea to have flexibility, especially for real estate investors who will draw off and you will pay off the HELOC a couple of times throughout buying numerous attributes.

Should you sign up for a home collateral loan to acquire a taxation deduction?

Zero, cannot remove a house equity mortgage just for brand new tax deduction. For folks who have a property guarantee loan, you may be able to get an income tax deduction to your desire portion of the loan providing you make use of the financing proceeds to help you buy, make or substantially improve the home you to definitely obtains the mortgage. Understand that this simply benefits your for people who itemize your income tax write-offs. By using the quality deduction, you will see no benefit to having a house equity loan to possess taxation intentions.

Was a property collateral mortgage a great hedge up against occupations losses?

No. Property security loan needs you to definitely make money after getting you to definitely away. Ergo, scraping your home’s security to get cash prior to a possible layoff has actually limited electric.

What can domestic equity mortgage proceeds be used having?

You are able to your home guarantee mortgage continues toward anything you wanted. Only the common sense are commercially stopping you from putting all of it into the black at the regional roulette desk. This is why it’s important to understand the risks or take away a house security financing diligently.

The bottom line

Like other almost every other financing items, a home security mortgage are going to be smart in a few factors and you will a poor tip in others. See the dangers and you may think whether risking your home is well worth any you are taking the actual mortgage to have. Generally, you really need to merely think property collateral loan to possess something which can increase their home’s worth.